Executive Summary

Over 1 billion users currently need assistive technology. This figure is expected to reach 2 billion by 2050 as the population ages and consumer electronics and assistive products converge. The market is shaped not only by demographics and the demand for consumer electronics, and the investment this attracts, but by legislation and policies. The Convention on the Rights of Persons with Disabilities (CRPD) recognizes access to assistive technology as a human right, bringing with it state obligations and expected market influence. Data shows that emerging products are usually not replacing conventional assistive products, but complementing them[1]. And as these assistive technologies improve, so do people’s lives.

What are prosthetic devices?

A prosthetic device an “artificial device to replace or augment a missing or impaired part of the body”.[2] Although modern medicine and advancements in assistive technology may paint prosthesis as a product of later scientific developments, the use of artificial limbs to better human function dates back as early as 1,600 B.C. The use of an artificial toe around the foot of a Mummy dating back between 950 B.C. to 710 B.C.[3] confirms the fact that prosthesis has been around for ages. History is replete with examples of prosthetic devices even before the advent of modern medicine such as Barbarossa’s silver arm, Gotz of the Iron Hand and many more.

Prosthesis thereby play a vital role in helping people live a life of normalcy. Not only do prostheses help in functionality, but they also hold sociological importance. They help overcome the social stigma around this subject by giving users a new chance at life through artificial means. It is for this reason that they are also known as rehabilitation devices.

Today, technology has infiltrated every aspect of our lives, especially the medical industry. Prosthesis is one such industry that has profited tremendously due to the onslaught of cutting-edge technology and artificial intelligence. Earlier what were made with harnesses and knee lock controls, prostheses now are specialised based on every patients requirements and are equipped with assistive controls that follow realistic commands such as moving one’s fingers, making fists, pinching, etc.

It’s a heady time to be involved in prosthetic technology and development – one marked by quantum leaps in research and understanding how human bodies, and brains, work. From artificial limbs to exoskeletons, the field of prosthetics is exploding with new technologies designed to improve the quality of life for patients. The technology used for prosthetic limbs now includes 3D printing, device implants, digital design tools, and more. As scientists learn more about how the human body functions, prosthetic limbs will start to feel and behave like the real thing[4].

Presently, research in prosthetic technology primarily focuses on:

- 3D-Printed Prosthetics,

- Thought-Controlled Prosthetics to restore the sensation of touch,

- Neuroprosthetics,

- Brain activity mapping,

- Ambionics Tests

Applications and types of prosthetic devices

Since prosthetic devices are essentially substitutes for actual body parts, their most important application is to replace, correct or support a body part. There exist a variety of prostheses in the market today. Based on the positioning of the device, i.e., upper extremity or lower extremity, there exist different types of devices. There are also active and passive prostheses: active prostheses perform actual movement and bodily function while passive prostheses serve artificial purposes.

There are broadly three types of upper extremity prostheses:[5]

- Transradial prostheses: Transradial prostheses attaches below the elbow. These can be either active (powered by myoelectric signals or cables connected to the body) or passive.

- Transhumeral prostheses: Transhumeral prostheses is connected above the elbow but below the shoulder. Since they replace a majority of the arm, they are more complicated to make as they compensate for a missing elbow as well. They too come in active or passive forms.

- Silicon hands, fingers, and arms.

For the lower extremity prostheses, there broadly exist two types:[6]

- Transtibial prostheses: These attach below the knee and their primary function is to distribute the weight as the mobility of the leg remains due to the presence of the knee. Most patients require rehabilitation with this kind of prostheses as the foot usually doesn’t move.

- Transfemoral prostheses: Transfemoral prostheses are the most complicated of the aforementioned prostheses as they replace a majority of the leg by attaching above the knee but below the hips. In this case, there is a special socket mechanism designed to replicate the structure of the knee thereby giving mobility to the user. Patients in this case too require rehabilitation before they can fully use their prosthetic leg. The prosthetic socket is the main connection between the prosthetic limb and the residual limb which distributes the forces through the residual limb.

Prosthodontics is a branch of dentistry that deals with prosthetic devices designed for the purpose of replacing missing or damaged teeth. Prosthodontics is becoming highly relevant with the advent of Artificial Intelligence (AI) which is being deployed to enhance the industry. There are four branches of prosthodontics. These are:

- Fixed prostheses: These are permanent prosthodontics and include devices such as crowns, bridges, onlays, inlays and veneers.

- Removable prostheses: These are designed to last for long periods of time subject to replacement or removal for cleaning. They are not fixed but fitted. Examples include dentures and gingival veneers.

- Implant prostheses: These implants such as small titanium cylinders are designed to hold the prosthetic device in place to secure their position inside the mouth.

- Maxillofacial prostheses: These focus on correcting malformed or missing tissues that may be congenital (acquired from birth) or may be a result of an injury, illness or disease. These can be intra-oral (inside the body) such as palate covers, palate lifts, jaw replacements, etc. or extra-oral (outside the body) such as eye (ocular, orbital), ear (auricular), radiation shields, etc.[7]

The Working and Science behind prosthetics

The documentation of limb amputations and availability of prostheses is scarcely documented.

However, statistics from the USA show that 41,000 persons live there with substantial upper-limb absences. In addition, 5-6,000 major limb amputations are performed in England each year with around a fifth of these involving the upper limb[8].

With more research and development in the field of prostheses, multiple ways of making artificial limbs have been devised. More recently, the integration of sophisticated technology is one of them. This includes AI (Artificial Intelligence) aided prosthetic limbs. The prosthesis is first used on the functioning arm. The AI integrated in this learns and remembers the actions of this arm which is then attached to the phantom arm. AI has made possible incredibly accuracy of limb movements such as pinching and naturalised the whole process for the user.

Another popular prosthesis mechanism is the mind-control prosthesis or the brain-computer interface integrated neuroprosthesis which can recognize real-time data as well as learn virtual functions.

Prosthetic limbs are made from materials lighter than the conventional ones such as wood and plastic. Prosthetic companies now use urethanes, silicone, and mineral-based liners to improve the product flexibility and comfort. This contributes to the prostheses’ flexibility which has fuelled the global artificial limbs and body parts industry.

The major types of Prosthetics include:

- Upper Extremity

- Lower Extremity

- Liners

- Sockets

While the primary Modular Components are:

- Orthotics Upper Limb

- Lower Limb

- Spinal

The Market Players

Newly released Prosthetics and Orthotics Market analysis report by Future Market Insights shows that global Prosthetics & Orthotics Market sales in 2022 were held at US$ 6.5 Billion. With a CAGR of 6% from 2023 to 2033, the market is projected to cross US$ 12 Billion by 2033. The market through Orthotics is expected to generate significant revenue and is projected to grow at a CAGR of around 6% from 2023 to 2033.[9]

| Attribute | Details |

| Global Prosthetics and Orthotics Market (2023) | US$ 6.8 Billion |

| Global Prosthetics and Orthotics Market (2033) | US$ 12.2 Billion |

| Global Prosthetics and Orthotics Market CAGR (2023 to 2033) | 6% |

| USA Prosthetics and Orthotics Market CAGR (2023 to 2033) | 5.6% |

As per the Prosthetics & Orthotics Market research by Future Market Insights – a market research and competitive intelligence provider, historically, from 2018 to 2022, the market value of the Prosthetics & Orthotics Market increased at around 5.3% CAGR[10].

Some factors that influence the Prosthetics & Orthotics industry include the increased frequency of neurological disorders and cardiovascular diseases that damage the patients’ neural and spinal systems. As discussed in section 2.3 of this report, the technical advancements in the prosthetics industry are to play a huge role in influencing the industry. Furthermore, the rise in number of trauma cases is expected to boost the orthopaedics industry. The influence of phantom limb pain and residual limb pain due to the prolonged usage of prosthetics devices has increased in users thereby giving way for newer, better technologies to replace them.

The key providers of prosthetics and orthotics include Ossur, Blatchford, Inc., Fillauer LLC, Otto bock Healthcare GmbH, The Ohio Willow Wood Company, Ultraflex Systems, and Steeper Group.[11]

Endolite announcing its fully integrated, microprocessor-controlled lower limb system Linx that has been awarded the German Design Award in the Universal Design Category in October 2022 is a notable development amongst the Prosthetics and Orthotics providers.[12]

The Market Dynamics

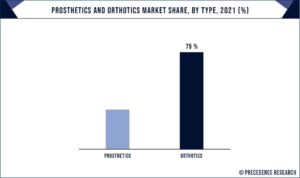

The global prosthetics and orthotics market is categorized into orthotics and prosthetics on the basis of their types. The orthotics market holds the largest revenue share of around 75% in 2021, due to the increase in the prevalence of osteoarthritis, sports injuries and the penetration of orthopaedic technologies.[13] The dominance of the orthotics sector can be attributed to the fact that they are recommended for fixing or accommodating foot deformities, aligning and supporting the ankle or foot. Further, the increase in recorded number of spine injuries and the cumulative occurrences of osteoarthritis are additional factors contributing to the increasing sales of orthotics. These solutions also offer tremendous potential in minimizing pain and addressing physical and postural problems.

Prosthetics type is sub-divided into modular components, liners, lower extremity, and upper extremity. The prosthetics market is anticipated to witness substantial growth in the years to come due to the upsurge in disability rates globally. Some prominent manufacturing companies in this industry include Zimmer Biomet Holdings Inc., Ossur HF and Blatchford Inc. According to the report published by the Rehabilitation Research and Training Centre on Disability Statistics and Demographics, in 2018, the percentage of people with disabilities in the United States increased from around 11.9% in 2010 to 12.9% in 2017, thereby leading to increasing demand for prosthetics in the country[14]

Drivers: Rise in demand for orthotic devices – The demand for orthotics devices can be attributed to multiple factors. The ageing population, for instance, is more prone to suffer from ailments such as osteoarthritis, osteoporosis and more bone-injury related ailments. There is also an increase in sport-related injuries. Orthotic devices are great alternatives to surgical deformity repair and pain management. Furthermore, the technological advancements in the prosthetics and orthotics market are making the orthotic products more affordable and accessible. Thus, this rising demand is boosting the overall growth of the prosthetics and orthotics market during the forecast period.

Restraints: Lack of consumer awareness – Although there have many technological advancements in the prosthetics and orthotics sector, the lack of consumer awareness in developing and under-developed countries acts as a setback for the progress of this industry. Since these devices are used to reduce pain, people with orthopaedic disorders can utilise these devices. However, the lack of awareness poses as an obstacle to this.

Opportunities: Rising geriatric population – According to the United Nations, the global population of people aged 60 and more is predicted to grow to 2.1 billion to 2050. People over 60 are more prone to illnesses like osteoporosis and osteopenia, which increases the demand for orthopaedic solutions.[15] Thus, the growing senior population globally is one of the main causes of the increasing demand for prosthetics and orthotics in the world.

Challenges: Higher cost of orthotic devices – With technological advancements in this sector, the cost as well as demand for customized orthotic devices has increased. Due to their low cost and accessibility, pre-fabricated devices are still being extensively used despite the fact that customized orthotic devices offer more functionality. Nowadays, pre-fabricated orthotic devise are highly advanced and come in various types and ranges depending on the diseases and ailments they cater to. As a result, customized orthotics are finding it difficult to compete and this is one of the biggest challenges for the growth of the prosthetics and orthotics market.

The Industry Analysis: The IP Scenario

Patent Trends

Leading Assignees

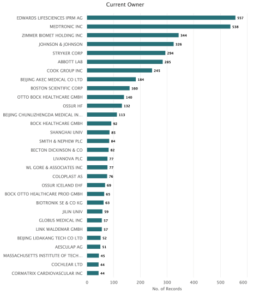

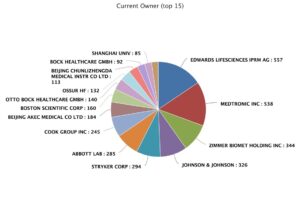

Edward Lifesciences dominates the prosthetic patent landscape with its aggressive filing of patent applications in tis domain and is closely followed by Medtronic Inc. Zimmer Biomet Holding, Johnson & Johnson, Stryker Corp, Abbott Lab, Cook Group Inc, Beijing Akec Medical Co Ltd, Boston Scientific Corp, Otto Bock Healthcare GMBH, Ossur HF and Beijing Chunlizhengda Medical also figures among the leading assignees.

Figure 3 showcases the graphical representation of patenting activity of the leading companies in this domain. Edward Lifesciences filed 557 patent applications in this domain in the last ten years and continued to be a major applicant over the years.

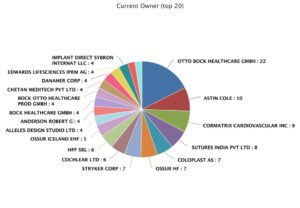

Bock Otto Healthcare Prod GMBH dominates the prosthetic design registration landscape in this domain and is closely followed by Austin Cole. Medtronic Inc., Zimmer Biomet Holding, Johnson & Johnson, , Stryker Corp, and Abbott Labs also figures among the leading assignees.

Edwards Life Sciences specializes in artificial heart valves and hemodynamic monitoring. Over the span of the last ten years, they have dominated the patent market by owning 4% of the total patents filed in this period. Medtronic Incorporation is an American company that develops and manufactures healthcare technologies. It comes at a close second by holding 3.9% of the patents in this industry. Other companies such as Zimmer Biomet currently hold 2.4% of the patents, Johnson & Johnson hold 2.3%, Stryker Corp 2.1%. These are the top 5 patent holders in this industry in the last ten years.

Patent Filing Trends

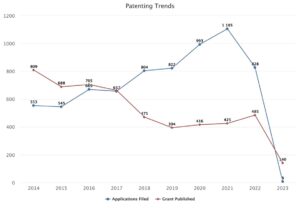

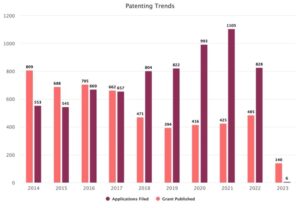

The number of patent applications filed in the prosthetics industry from 2014-2023 have seen an increase in the last few years peaking in 2021 at 1,105 applications. The trend saw a steep decrease in 2022, the lowest record in the last two years. The trends in grants published have been fluctuating with the highest number of grants published in 2014 at 809, and declining steadily since. 2022 saw a slight increase therefore becoming an anomaly in the trend with 485 grants published, the highest since 2017.

Geographical Patent Filing Trends

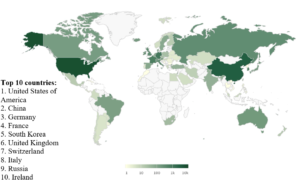

United States of America emerges as the leading country with 5,864 patents filed in the last ten years in the prosthesis industry.

Leading companies such as Edwards Life Sciences, Medtronic, Zimmer Biomet Holdings Inc., Stryker Corp, Abbott Laboratories, Cook Medical Group, Boston Scientific, etc. are based in the United States of America hence making it the world leader in this domain. China is US’s biggest competitor with 2863 patent filings in the last ten years. World players such as Beijing Akec Medical Co Ltd and Beijing Chunlizhengda Medical combined hold about 10% of the country’s prosthesis patents. Following China is Germany at 875 patents. Otto Bock Healthcare GMBH which places 10th on the list of market leaders hails from Germany and holds about 16% of the Germany’s prosthesis patents. France places 4th on the list with 606 patents, followed by South Korea at 454, United Kingdom with 379, Switzerland, Italy, Russia and Ireland. Israel, Australia, Iceland, Japan and Canada are emerging leaders in this domain.

Trends in various types of prosthetic devices

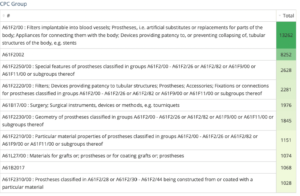

The highest number of patents are 13,262 and are filed in the CPC group filters implantable into blood vessels, prostheses, i.e., artificial substitutes or replacements for parts of the body, appliances for connecting them with the body, devices providing patency to, or preventing collapsing of, tubular structures, e.g. stents. This category broadly includes all kinds of prostheses patents filed in the last ten years. There are 8252 patents for implantable devices, 2682 for special features of prostheses that fall under other CPC groups. The total number of patents for prostheses filed in this period are 13,775.

Design Registration Trends

Leading Assignees

Otto Bock Healthcare GMBH is the global leader in design patent filings in the last ten years. The number of designs filed in the last ten years are significantly lower than the number of patents filed in the same period. This could be because design patents only cater to the appearance or configuration of the product and without any actual functionality or utility. Otto Bock Healthcare GMBH holds 8% of all design patents filed in the last decade. Following Otto Bock Healthcare is Austin Cole with 10 design filings. Other notable players are Cormatrix Cardiovascular Inc. based in the United States of America with 9 design filings, Sutures India Pvt. Ltd. based in India and Coloplast which is a Danish company specialising in developing ostomy, continence, interventional urology, wound and skin care products and services.

Some of the notable patent holders such as Edwards Life Sciences, Stryker Corp, Ossur HF and Otto Bock Healthcare come in the top 20 design holders as well, although their share is significantly lesser in this domain. Edwards Life Sciences merely holds 1.5% of the total design filings, Stryker Corp holds 2.6% same as Ossur HF.

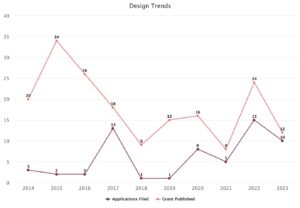

Design Filing Trends

The design filing trends from 2014-2023 show fluctuation throughout the period. The number of applications filed in this time period hit their second highest peak in 2017 (13) which was a steep increase from 2014. They then saw a significant drop in the years 2018 and 2019 with only 1 design application filed in both these years respectively. 2020 saw an increase in number to 8 applications which then decreased to 5 in 2021. The highest number of design applications were filed in 2022 at 15.

The trends in grants published show a similar fluctuation but more exaggerated. They highest number of grants were published in 2015 which were 34. From the years 2015 to 2018 they saw a steady decline to 9 grants published in 2018. There was a momentary increase from the years 2018 to 2020. 2021 saw the sharpest decline to 8, the lowest number of grants published in the last ten years in the prosthetics industry. However, the number of grants published showed a 200% increase in 2022.

Geographical Design Filing Trends

It is evident from the map above that designs have been filed in very few countries. Some countries such Russia and the African continent have registered zero designs from 2014-2023. The country with the highest number of design filings is the United States of America with 70 design filings which is around 27% of the total design filings in the last ten years. Second on this list is India with 34 design filings accounting to 13% of the total design filings in this period. Amongst the top market assignees, Sutures India Pvt and Chetan Meditech Pvt. Ltd. together make up 35% of the country’s design filings. Third on the list is Germany with 18 design filings. Otto Bock Healthcare that hails from Germany is the owner of maximum number of design filings in the last ten years. Following Germany is Austria with 16 designs (6%), Canada with 11 designs (4%), Iceland with 10 from Ossur HF holding 70% of the country’s design filings. Italy, United Kingdom, Japan and Australia make the top 10 countries in the world in the design filings in the prosthetics industry.

Current IP Scenario

The global orthopaedic prosthetics market will see a 4.5% increase by 2030, with upper extremity prostheses accounting for nearly two-thirds of the market share.[16] In 2022, 828 patent applications were filed and 485 were granted. The MedTech industry was already growing before the global pandemic, but after the COVID-19 pandemic of 2020, the highest number of patent applications were recorded in 2021. With the European Patent Office (EPO) introducing the Unified Patent System in June 2023 which will simplify the patent processes across EU[17], the current IP scenario appears to be going in a positive direction. This could be prosperous not only for the prostheses industry, but the entire global patent landscape.

Economic Analysis:

Impact of Patents and Design Filings on the Revenues of the Market Leaders

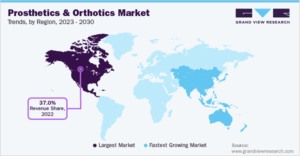

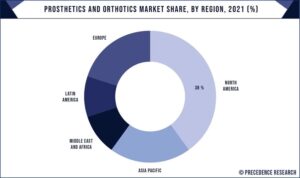

A significant share of the global Prosthetics & Orthotics market is held by North America as of 2022. Multiple factors such as increased awareness amongst the older populations about cardiovascular and neurological disorders as well as awareness about sports injuries contribute to this success. Additionally, support from the Government and the ease of accessibility to high-quality medical facilities and attractive reimbursement policies play a vital role in its success.[18]

In 2018, North America led the myoelectric prosthetics market, owing to a convergence of trends such as greater acceptance of new technologies, an increase in the number and instances of Critical Limb Ischemia, and higher investment in the area[19].

The global prosthetics and orthotics market is categorized into four key regions, comprising North America, Europe, Asia-Pacific, and the Rest of the World (RoW). North America accounted market share of around 38% in 2021.[20] Due to the presence of established prosthetic makers in the United States, the demand and growth of the prosthetics and orthotics market has been growing at an unprecedented rate. Due to the better proficiency and skill of medical experts, many choose to get their treatment from U.S. However, it is expected that the prosthetics and orthotics market in Europe and APAC will pick up pace during years to come[21].

How patents and design filings contribute to a company’s revenue and profits

Patents are valuable intangible assets of a company. They protect a company’s innovation for a limited period of time (20 years) granting them exclusive rights and access to that invention. It is therefore clear why a company would need to protect their intellectual property or innovations and inventions. It gives them a competitive edge in the market can help make the business more efficient. There are multiple ways through which patents and design filings and protections benefit a company’s revenue.

- Licensing and royalties: In an industry which thrives on innovation such as the medical technology and prosthetics industry, out-licensing patents is a very good way for companies to generate revenue. The income from out-licensing patented technologies may be in the form of royalties.

- Exclusivity: By patenting the technologies and inventions, companies can prevent third parties from making, using, selling, offering for sale or importing the patented inventions in the country(ies) where the patent is granted. This gives a competitive edge to the companies and they are able to prevent their competitors from making the same or similar products. This is used as a defensive strategy by big companies to avoid litigation for the same.

One of the most impending legal risks that companies face is their inability to safeguard their intellectual property. E.g., Edwards Life Sciences in their 2022 form 10-K list[22] “a, Inability to protect our intellectual property, b, Inability to defend against intellectual property claims property claims from third parties” as their biggest threats under Legal, Compliance and Regulatory Risks.[23]

Many companies such as Edwards Life Sciences, Zimmer Biomet, Johnson and Johnson etc. have stated in their financial statements that, “Our inability to protect our intellectual property or failure to maintain the confidentiality and integrity of data or other sensitive company information, by cyber- attack or other event, could have a material adverse effect on our business.”[24] Patents therefore play a vital role in ensuring the success and competitiveness of a company.

- Attracting investments and collaborations: When an invention is brought to the market to attract investors, it’s imperative that the invention is protected or else there is a risk of someone else copying it. In that case, an investor would not be interested in funding a project that can be done by other companies as well. Hence, patented and protected inventions serve as a measure of security which in turns boosts investments and collaborations.

- Company valuation: Patents not only serve as an apparent protection for companies but also carry monetary value for companies in the form of intangible assets. For example, as of December 31, 2022, the total value of Intellectual Property Rights of Zimmer Biomet was $137.7 million.[25] In the year 2022, the gross value of intangible assets such as patents and trademarks for Johnson & Johnson was $21,746 million.[26] For Medtronic Inc., in the year 2022 the gross carrying amount of purchased technologies and patents was $10,802 million and $473 million for trademarks and tradenames.[27]

The aforementioned statistics of some of the largest patent holders in the prosthetics industry shows how important it is for a company to safeguard their intellectual properties and technologies which can in turn yield huge revenues.

Revenue from Prosthetics and market leaders

In the previous section of this report, we had discussed the leading patent owners in the prosthetics industry. They are as follows:

- Edwards Life Sciences: Edwards Life Sciences ranks #1 as the holder of maximum number of patents in this industry. Headquartered in Irvine, California, Edwards Life Sciences was founded in 1958 and specializes in artificial heart valves and hemodynamic monitoring.[28] It’s net revenue in 2022 was $5,382.4 million (Form 10-K).

- Medtronic Inc.: Ranking #2 in the list of global leaders in the prosthetics industry, Medtronic Inc. currently is the owner of 538 patents of prosthesis. Headquartered in Minneapolis, Minnesota, Medtronic is a global leader in developing and manufacturing healthcare technologies.[29] It’s net revenue in 2022 was $31,686 million (Form 10-K).

- Zimmer Biomet: Zimmer Biomet was founded in 1927 and is headquartered in Indiana, United States of America.[30] It’s revenue in the year 2022 was $6,960 million (Form 10-K).

- Johnson & Johnson: Johnson & Johnson is a multi-national corporation in the consumer health, pharmaceutical and MedTech industry. It was founded in 1886 and is headquartered in New Jersey, United States of America.[31] In 2022, it’s net sales were $94,943. (Form- 10K)

- Stryker Corp: Stryker is one of the world’s leading medical technology companies and specialises in medical and surgical equipment, orthopaedics, neurotechnology and training and education.[32] It made a revenue of $18,449 million in 2022. (Form 10-K)

- Abbott Laboratories: Headquartered in Illinois, United States, Abbott Laboratories is a multinational company founded in 1888. It primarily specializes in medical devices and healthcare. It’s revenue in 2022[33] was $43,653.00 million. (Form 10-K)

- Cook Medical Group: Cook Medical is based in Bloomington, Indiana, United States and is primarily involved with the manufacturing of medical devices.[34]

- Beijing Akec Medical Co Ltd.: Beijing AKEC Medical Company Limited develops, manufactures and sells orthopedic medical device products. The Company’s main product is artificial arthroplasty, which includes artificial knee joints, and artificial hip joints products. It’s net sales in 2022[35] were $73.31 million.[36]

- Boston Scientific Corporation: Boston Scientific is an American Company that specialises in endoscopy, interventional cardiology, neuromodulation, peripheral interventions, rhythm management, urology and pelvic health.[37] It’s annual revenue in 2022 was $12,682.00 million. (Form 10-K)

- Otto Bock Healthcare GMBH: Otto Bock GMBH is world leader in the prosthetics industry and is based in Duderstadt, Germany. It specialises in orthopaedics, wheelchairs, exoskeletons and prosthetics. It’s annual revenue in 2022 was 1.3 billion euros.[38]

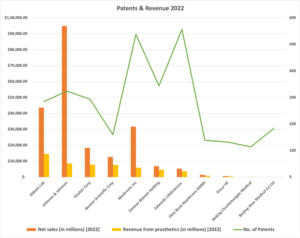

Revenue distribution in the prosthetics industry

| Patent Rank | Market Leaders (current owners) | No. of Patents | Net sales (in millions) [2022] | Revenue from prosthetics (in millions) [2022] | % revenue from prosthetics |

| 1 | Abbott Lab | 285 | $43,653.00 | $14,687.00 | 33.64% |

| 2 | Johnson & Johnson | 324 | $94,943.00 | $8,587.00 | 9.04% |

| 3 | Stryker Corp | 294 | $18,449.00 | $7,838.00 | 42.48% |

| 4 | Boston Scientific Corp | 160 | $12,682.00 | $7,705.00 | 60.76% |

| 5 | Medtronic Inc | 538 | $31,686.00 | $5,908.00 | 18.65% |

| 6 | Zimmer Biomet Holding | 344 | $6,940.00 | $4,673.20 | 67.34% |

| 7 | Edwards Life Sciences | 557 | $5,382.40 | $3,634.30 | 67.52% |

| 8 | Otto Bock Healthcare GMBH | 139 | $1,445.60 | $834.18 | 57.70% |

| 9 | Beijing Akec Medical Co Ltd | 184 | $73.31 | $73.31 | 100.00% |

| 10 | Cook Group Inc | 245 | $2,236.00 |

Many of these companies specialize primarily on developing and manufacturing prosthetic devices such as Zimmer Biomet Holding, Beijing Akec Medical Co. Ltd. And Otto Bock Healthcare GMBH. Other companies such as Johnson & Johnson, Medtronic Inc, etc. specialize in many other fields of medical sciences.

| S. No. | Market Leaders (current owners) | No. of Patents | Net sales (in millions) [2022] | Revenue from prosthetics (in millions) [2022] |

| 1 | Edwards Life Sciences | 557 | $5,382.40 | $3634.3 |

| 2 | Medtronic Inc | 538 | $31,686.00 | $5,908 |

| 3 | Zimmer Biomet Holding | 344 | $6,940.00 | $4,673 |

| 4 | Johnson & Johnson | 324 | $94,943.00 | $8,857 |

| 5 | Stryker Corp | 294 | $18,449.00 | $7,838 |

| 6 | Abbott Lab | 285 | $43,653.00 | $14,687 |

| 7 | Cook Group | 245 | $2,336 | |

| 8 | Beijing Akec Medical Co Ltd | 184 | $73.31 | $73.31 |

| 9 | Boston Scientific Corp | 160 | $12,682.00 | $7,705 |

| 10 | Otto Bock Healthcare GMBH | 139 | $1,445.6 | $834.18 |

It is observed that Abbott Laboratories that rank #6 globally in the prosthesis patent market yielded the maximum revenue of $14,687 million in the year 2022. The prostheses products constitute nearly 1/3rd of the company’s total revenue. Second in the list is Johnson & Johnson, making $8,587 million from medical devices and prostheses alone. This sector only makes up 9% of the total revenue of the company. Stryker Corp places third with 42% of their revenue coming from prostheses valued at $7,838 million. Boston Scientific Corp is a close fourth after Stryker Corp, closing in at $7,705 million which is nearly 61% of their total revenue. Medtronic Inc, despite being the second largest prostheses patent holder places 5th on the list of revenue from prostheses which constitutes 18% of their total sales. Interestingly, Edwards Life Sciences which owns the largest number of patents in this industry places 6th on the list of prostheses revenues despite prostheses constituting 67.5% of their total revenue. Otto Bock Healthcare GMBH, the world leader in prostheses design filings places 8th on the revenue list. Beijing Akec Medical Co. and Zimmer Biomet are close competitors as well.

Contribution of Patents and Designs for the Market Leaders

As stated in section 4.1 of this report, patents and designs play a huge role in ensuring the success of a company. Patents, designs, trademarks are usually listed as intangible assets in a company’s financials, but they are assets, nonetheless. Patents and designs also indirectly increase the monetary value of companies. They do this by increasing the goodwill and trust of consumers in the respective companies, they can be used in out-licensing of patented technologies and enabling organizations and companies to enforce their rights.

- Edwards Life Sciences:

In Edwards Life Sciences form 10-K for the year 2022, it is observed that the company invested $205.5 million in patents, which are finite-lived intangible assets. This is an increment from 2021 by about $20 million. The net carrying value of the patents at the end of 2022 is $20.5 million, about thirteen times more than 2021. This indicates that Edwards Life Sciences understands the importance of investing in patents and safeguarding their intellectual property which will yield great revenues in the future.

- Medtronic Inc.

For Medtronic Inc., in the year 2022 the gross carrying amount of purchased technologies and patents was $10,802 million and $473 million for trademarks and tradenames. The high investment in purchasing technology and patents is highly beneficial for the company as it can help them expand their existing product/innovation line and contribute in research and development.

- Zimmer Biomet Holdings

Zimmer Biomet’s intangible assets such as Intellectual Property Rights are valued at $137.7 million and trademarks and tradenames at $711 million. This is a decrease from 2021 owing to the increase in amortization of the intangible assets. Trademarks and tradenames constitute 14% of the total value of intangible assets of 2022.

- Johnson & Johnson

There is a positive trend in the patents investments from 2021 resulting in greater values for patents and trademarks. Johnson & Johnson is a multinational corporation with maximum focus on consumer health products, therefore It realizes the importance of protecting its innovations in this incredibly competitive industry.

For the global leaders, protecting their technologies is extremely vital. Stryker Co. in 2022 had intangible assets (patents + trademarks) worth $251 million. Not only do patents ensure security but the mere investment in patenting technologies is an important factor to consider while ascertaining the company’s commitment to its successful future

Linking the Revenue to Patents and Designs

The trends are very inconsistent and there is no linearity observed between the patents filed and the revenue generated. Edwards Life Sciences, the largest patent holder generated minimal revenue from prosthesis. This could mean that the company has filed multiple patents to avoid other companies to use the same technology, or to increase their brand value and marketing without any actual utility of those patents. Further, these patents could be utilised in the future to generate larger revenues.

The annual revenue of Edwards Life Sciences is also in the lower half of the top 10 companies which could signify that the company is not investing the right amount of resources or facilities to yield the complete potential of their prostheses patents. This could be a risk to the business as 2/3rd of the revenue is generated by prostheses thereby making it an integral part of their business.

Abbott Labs have made the most revenue from their prosthetic devices with nearly 34% of their business coming from this sector. This is a sharp contrast from Edwards’ financials which hold almost double the number of patents and yields almost one-fifth the revenue of Abbott Labs from prostheses.

Johnson & Johnson has the highest annual revenue amongst all companies and second highest revenue from prostheses. Prostheses contribute only 9% of the company’s revenue and yet places second. Johnson & Johnson does not specialise in prostheses as compared to its other competitors such as Otto Bock Healthcare and yet performed exceptionally well.

There is also a disparity in Medtronic Inc.’s prostheses patents and revenue generated. 18% of Medtronic’s revenue comes from prostheses.

Litigation in the Prosthetic Devices Industry

After the COVID-19 global pandemic, the MedTech industry has becoming increasingly relevant. Recent patent filings have been primarily focused on information and communications technology (ICT) specially adapted for medical diagnosis such as point-of-care devices, wearables, and remote monitoring systems such as telemedicine, medical simulation, or medical data mining followed by surgical robots.[39] With Artificial Intelligence (AI) becoming extremely prevalent in almost all sectors and industries, its introduction in the MedTech and especially prosthetics industry is notable. Recent technologies with the help of AI are aiming to revolutionise the current models of prosthetic devices. In built AI systems in the devices will learn the movements of the functioning body part which they will then remember and replicate. This will then be installed in the phantom body part as a prosthetic device. This does away with the previously used myoelectric and body connected prosthetic devices.

With an increase in innovation and patent filings in this industry, there have been litigations and oppositions as well.

Disputes in the Industry

In the last ten years, there have been multiple oppositions and litigations in the prosthetics industry. Some of these involve the biggest players in the industry such as Edwards Life Sciences, Zimmer Biomet, Cook Medical, etc. Listed below are the legal proceedings and disputes in the industry amongst the biggest players. Some notable disputes are as follows:

- Edwards Life Sciences v. Abbott Laboratories

In 2019, Abbott Laboratories alleged Edwards’ transcatheter valve repair system Pascal infringes on its MitraClip patents in lawsuits filed in the U.S. and several European markets.[40] In 2020, Edwards Life Sciences agreed to pay Abbott $368 million upfront to settle disputes over patents for transcatheter mitral and tricuspid valve repair products, plus roughly $100 million in royalties through mid-2024.[41] This led to Edwards Life Sciences spending approximately $405 million on intellectual property related litigation settlements in 2020.[42]

At present, Edwards Life Sciences is in a legal proceeding led by Aortic Innovations LLC in 2021 alleging that Edwards’ SAPIEN 3 Ultra product infringes certain of its patents.[43]

- Stryker Corp v. Conformis

Stryker Corp acquired Wright Medical in November 2021. Conformis alleged that many patient-specific devices made by Wright Medical infringed upon their patents. In this dispute, Stryker Corp had to pay $15 million to Conformis.[44]

- NuVasiv v. Medtronic

The lawsuit was initially filed in 2008 regarding spinal products, and in 2016 both companies agreed mutually to settle the lawsuit for $40 million paid by NuVasiv to Medtronic Inc.

Opposed Patents

There have been multiple oppositions to patent applications and grants in the last ten years. Most of the oppositions have been recorded from the European Patent Office, followed by United States, South Korea and Germany.

- EP898943B1: Dental Prosthetic Part[45]

Applicants: WIELAND DENTAL & TECHNIK GMBH [DE]

On 2004-08-12, opposition was filed by DENTALES SERVICE ZENTRUM GMBH & CO.KG post-grant.

- EP3400908B1: Artificial Valve Prostheses[46]

Applicants: COOK MEDICAL TECHNOLOGIES LLC [US]

On 2021-04-28, opposition was filed by NEOVASC TIARA INC. in Germany after the patent was granted.

- EP2982337A1: Paravalvular Leak Detection, Sealing, and Prevention[47]

Applicants: EDWARDS LIFESCIENCES PVT INC [US]

On 2021-05-25, opposition was filed in Germany. On 2021-06-29, opposition was filed in Finland by ABBOTT CARDIOVASCULAR SYSTEMS, INC. and NEOVASC TIARA INC.

On 2021-06-30, both companies filed oppositions.

On 2023-06-30, date of receipt of notice of appeal recorded. This was the latest legal development in this case.

- EP2962726A1: System for excitation of phantom sensations[48]

Applicants: MEIER-KOLL ALFRED [DE]

On 2021-08-03, opposition against patent was filed in Germany by SAPHENUS MEDICAL TECHNOLOGY GMBH.

On 2023-06-03, opposition was rejected.

- EP2720648B8: Femoral Component for a knee prosthesis with improved articular characteristics[49]

Applicants: ZIMMER INC [US]

On 2016-06-08, opposition was filed by SLINGSBY PARTNERS LLP. The appeal procedure was closed on 2021-11-17. On 2022-09-13, the patent was revoked following opposition.

- US9907561B2: Ankle replacement and method[50]

Original Assignee: WRIGHT MEDICAL TECH INC (US)

Current owners: STRYKER CORP (upon acquiring WRIGHT MEDICAL), WRIGHT MEDICAL GROUP NV.

- KR20180122237A: Apparatus for exercising prostatic hyperplasia by neural stimulation[51]

Applicants: PARK JEONG HOON (KR)

On 2019-01-31, the decision to refuse the application was passed.

Legal status: Inactive-rejected/ refused/ suspended

Corporations and companies expend certain sums of money per annum for settlements to counter oppositions and litigation claims. Many of these patents cease to exist due to fierce oppositions. The patents listed above are a few of many oppositions filed in the last ten years and is not exhaustive.

Litigations

While there have been many patent oppositions, the litigations in this industry are also many in number. There have been a total of 20 litigations in the last ten years, some of which have costed big corporations huge sums of money owing to patent infringements. Some of these have been listed in section 5.1. 14 out of these 20 litigations have been from US patents and the rest are from China and Japan.

- US8623077B2: Apparatus for replacing cardiac valve.

This patent was published on 07-Jan-2014 by Medtronic Inc. A petition was filed by Edwards Life Sciences in 2014 in the United States Patent and Trademark office before the Patent Trial and Appeal Board. The petitioner, Edwards Life Sciences requested for a review of certain sections of the publication filed by Medtronic Inc. due to non-distinctness of their existing products. The final decision has not been decided yet.[52]

There have been multiple litigations between these two companies in the past regarding transcatheter aortic valve replacement systems. In 2010, a $73 million judgement in favour of Edwards was regarding similar products. Another case’s recent ruling in January 2014 for nearly $394 million in favour of Edwards in a case against Medtronic.[53]

- US9393110B2: Prosthetic Heart Valve.

This patent was published on 19-July-2016 by Edwards Life Sciences who is the current owner. Edwards was the plaintiff that alleged that the defendant Meril Inc was attempting to capitalize on Edwards’ success by infringing multiple Edwards’ patents, designs, innovations and trademarks. Although both corporations had settled their dispute by paying settlement money, a court ruling dated May 18th, 2022 held in favour of the plaintiffs and against Edwards. [54]

- US9492280B2: Multiple-cam, posterior-stabilized knee prosthesis.

This patent was published on 15-Nov-2016 by MEDIDEA LLC. In the same year, the plaintiffs MedIdea brought a case against the defendants DePuy Orthopaedics Inc. for patent infringement. The United States District Court of Massachusetts ruled in favour of the defendants DePuy orthopaedics and against MEDIDEA LLC. The patent is currently terminated.[55]

JP2018519868A is a litigated patent for palm unit for artificial hands by ハイファイブプロ エーエス, a Japanese company. Some Chinese patents are as follows: CN104207863B (Introduce the total joint replacement prostheses of torque), CN102098984B (Anchoring of tendon f biceps of prosthetic device under arthroscope), etc.

Mergers and Acquisitions

There have been many significant acquisitions in for the top players in the industry.

- Edwards Life Sciences

Edwards Life Sciences did not acquire any companies in 2022. Its latest acquisitions include Corvia Medical in 2019 for $35 million and CAS Medical Systems in the same year for $100 million. The largest acquisition done by Edwards was in the year 2015 when it acquired CardiAQ Valve Technologies, Inc. for $400 million. Sector-wise, 77% of their total acquisitions come from the medical products sector, followed by life sciences (8%). Totally, they have acquired 13 companies (add-on acquisitions and divestitures). [56]

- Medtronic Inc.

Medtronic Inc. has acquired a total of 62 companies. It’s latest acquisition is of EOFlow (2023) which is a South-Korean medical device company for $738 million.[57] In 2022, it acquired Massachusetts-based Affera, a medical technology company specialising in innovations related to cardiac arrhythmia for $925 million. Medtronic’s biggest acquisition till date is of Covidien PLC for $42.9 billion in 2014.

Sector-wise, 58 companies acquired are from the medical products sector (88%). 7% is from healthcare services and 2% is from life sciences.[58]

- Zimmer Biomet Holdings:

Zimmer Biomet Holdings has acquired 24 companies. It’s largest acquisition was of Biomet Inc. for $13.3 billion in 2014. It’s latest acquisitions include A&E Medical Corp in 2020 for $250 million.[59] In 2022, it had reached a definitive agreement to acquire Embody Inc. for $155 million and up to an additional $120 million subject to achieving future regulatory and commercial milestones over a three year period.[60]

- Johnson & Johnson:

Johnson & Johnson has acquired a total of 41 companies. It acquired Abiomed in 2022 for $16.6 billion. It’s largest acquisition was of Actelion Ltd., a biopharmaceutical company for $30 billion in the year 2017. In 2011, it acquired Synthes Inc. for $19.3 billion. 39% of the companies acquired by Johnson & Johnson are from the medical products industry. A close second is the life sciences industry (37%) followed by consumer products (12%) and digital media (5%). [61]

- Stryker Corp:

Stryker Corp has acquired a total of 44 companies. It’s most recent acquisitions include Vocera in 2022 for $3 billion and Gauss Surgical in 2021. It is to acquire Cerus Endovascular in 2023. It’s largest acquisition was in 2019 when it acquired Wright Medical Group N.V. for $5.4 billion. It’s highest acquisitions have been in the medical products sector (75%), followed by healthcare services (14%) and manufacturing (7%).[62]

- Abbott Laboratories:

Abbott Laboratories acquired Cardiovascular Systems Inc. in February 2023 for $890 million. Their total number of acquisitions are 34. Their biggest add-on acquisition was of St. Jude Medical Inc. in 2016 for $25 billion. 56% of these acquisitions are from the medical products industry, followed by Life Science (32%) and information technology (3%).[63]

- Boston Scientific:

Boston Scientific Corp has acquired a total of 62 companies with its most recent acquisition being Acotec in 2022. Its biggest acquisition was of Guidant Corp. in 2006 for $24.6 billion. 77% of their acquisitions are in the medical products industry, followed by health care services (13%) and life sciences (8%). [64]

The Future

The future of the orthotics and prosthetics industry looks promising. This report has substantiated this point through analysing various patent trends and industry analysis. It is expected that the orthotics market will grow significantly in terms of revenue in the next ten years. Orthotics is forecasted to grow at the highest CAGR of over 5.9% from 2023 to 2033.[65]

As discussed earlier, cardiovascular, neural and bone-related ailments have increased in the projected period therefore increasing the demand for orthotics and prosthetics. Additionally, diabetes-related amputations are also becoming common globally, further increasing market growth. Orthotics can be used in conjunction with physiotherapy procedures such as muscular training and stretching, gait and balance retraining, and reach and grip tactics to help patients achieve their goals[66].

The USA is expected to account for a significant market of US$ 3.7 Billion by the end of 2033.[67] This can be attributed to the fact that most of the major players in this industry such as Edwards Life Sciences, Zimmer Biomet Holdings, Medtronic, Johnson & Johnson hail from the U.S. The proficiency and skill of the region’s medical specialists and doctors have motivated people from other locations to travel there for prosthetic and orthotics treatments. According to the National Limb Loss Information Centre, approximately 1.7 million people in the USA have lost a limb for whatever reason.[68] According to some estimates, one out of every 200 people in the USA has had a limb amputated.[69]

The market in the UK is expected to reach a valuation of US$ 522 Million by 2033, growing at a CAGR of over 5% from 2023 to 2033. During the forecast period, the market is projected to witness an absolute dollar opportunity of US$ 218 Million.[70]

In Japan, the market is projected to gross an absolute dollar opportunity of US$ 320 Million from2023 to 2033, growing at a CAGR of 8.3%. By 2033, the market is projected to reach US$ 583Million.[71]

The Indian scenario is different. Due to the economic disparities amongst the people of India, the affordability of prosthetics is the biggest challenge in this industry. High-end prosthetic devices cost lakhs and the cheaper alternatives offer limited functionality. According to reports, India has more than half a million amputees, with tens of thousands added to the amputee population every year.[72] However, this is expected to change with Indian prostheses start-ups such as Robo-Bionics, Chetan Meditech, etc. making great strides in this field.

Conclusions

Amputations are done on an estimated 158,000 people in the USA each year, with the absolute number of amputations growing. For upper-limb amputation, reported rates of prosthesis use range from 27% to 56%, while lower-limb amputation rates range from 49% to 95%. The industry is expanding due to the rising desire for custom-made foot orthotics[73].

This report sheds light on the current IP scenario of the prostheses industry. The patenting trends are on an increase especially after the COVID-19 global pandemic, indicating a positive trend. However, we have also observed that the number of patents filed by a company is not necessarily proportional to the revenue generated. Amongst the largest patent holders, there is a need to maximise the potential from these patents to maximise revenues.

There has also been an uptick in the number of design filings, with several Indian companies becoming relevant in this context. Geographically, the United States dominates both patent and design filings from the trends observed in the last ten years.

Technological advancements have been accelerated in the last decade. This has led to the development of Artificial Intelligence-based prostheses amongst others. This has the potential to completely revolutionarise the industry. Some other key developments include the advent of neuromuscular signal processing.

3D printing is another important driver in the development and manufacturing of prosthetic devices. It plays an incredibly vital role in simplifying the process of creating customised prosthetic limbs and devices. The traditional orthotic solutions are generic therefore the boosters of this industry are the customisable prosthetics that provide patients more comfort. 3D printing aids this.

Authors: Prof (Dr) Anindya Sircar (DPIIT Chair Professor; NALSAR University of Law, Hyderabad, India) and Ms Bhavya Sharma (BBA LLB Student, Jindal Global Law School, Sonipet, India)

Please contact us at info@origiin.com to know more about our services (Patent, Trademark, Copyright, Contract, IP Licensing, M&A of companies)

Subscribe to YouTube Channel HERE

Join LinkedIn Group: Innovation & IPR

WhatsApp: +91 74838 06607